1. Indonesia: The Leading Competitive Threat

Indonesia has emerged as Vietnam’s most formidable competitor in the South Korean market.

Current Market Situation

-

Overtaking Vietnam:

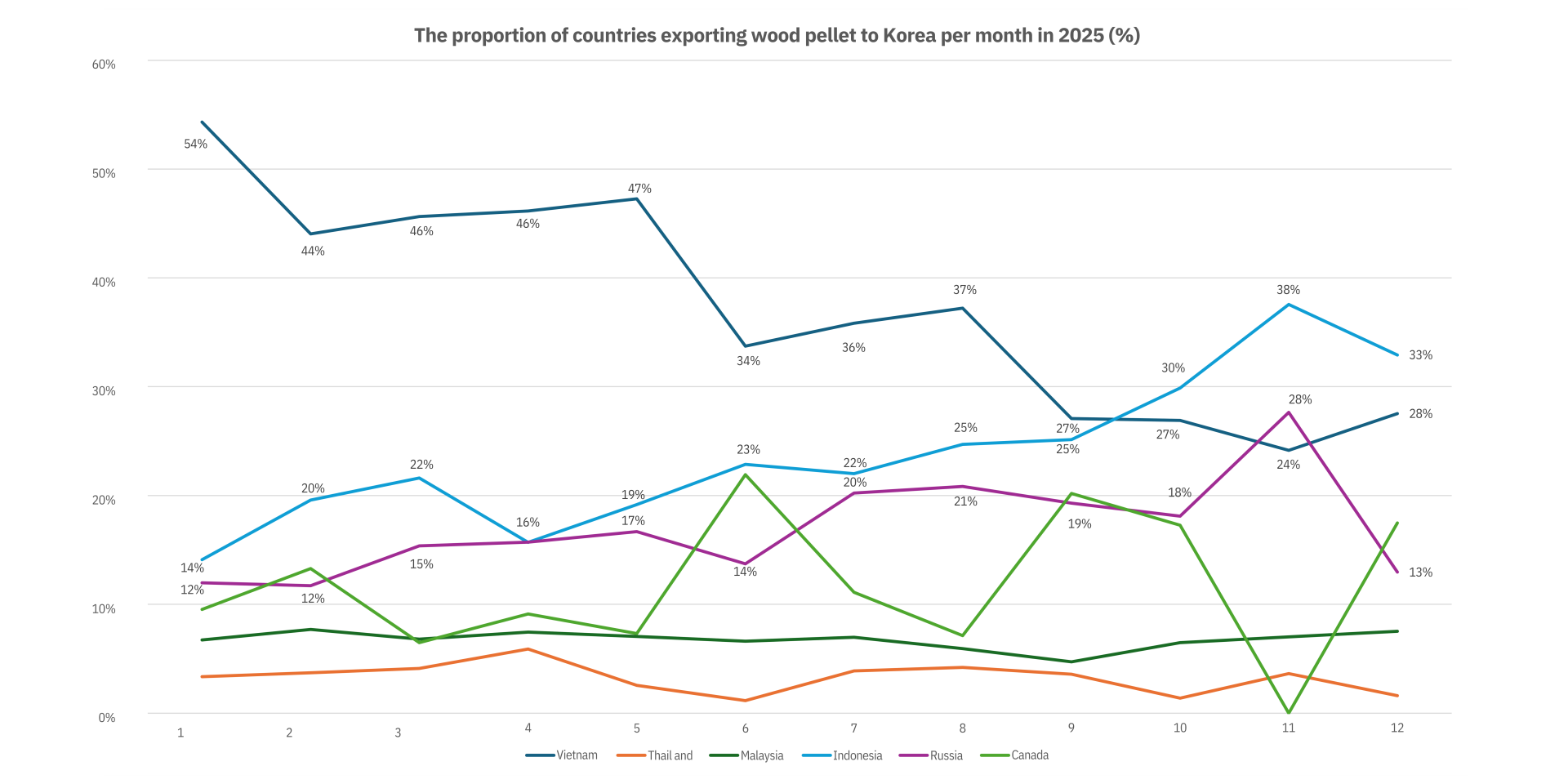

Indonesia overtook Vietnam to become the largest exporter of wood pellets to South Korea in November and December 2025, marking a sharp shift from the previous year.

In 2024, Vietnam exported 172,000 tons in November and 198,000 tons in December. By comparison, shipments fell dramatically in 2025 to 68,000 tons in November and 88,000 tons in December, representing a year-on-year decline of approximately 61% and 56%, respectively.

Meanwhile, Indonesia recorded strong growth over the same period. Exports to South Korea increased from 56,000 tons in both November and December 2024 to 105,000 tons in November 2025 and 106,000 tons in December 2025, equivalent to a year-on-year increase of roughly 88–89%.

-

Price Competitiveness:

Indonesian pellets have been winning tenders thanks to lower offer prices, while Vietnamese pellets are under pressure from rising production costs caused by raw material shortages. -

Quality Advantage:

South Korean buyers generally assess Indonesian pellets (along with Russian and Canadian pellets) as having better overall quality than shipments from Vietnam. Vietnamese cargoes are under heightened scrutiny and have faced rejections at Korean ports due to issues related to moisture content and impurities.

New Plants & Production Capacity (2026 Outlook)

-

G7 & BEG Joint Venture:

Polish trader G7 and Indonesia’s PT Biomassa Energy Group are planning six new plants. The first is a 120,000 tpa EFB pellet plant in Sumatra, expected to commence operations in 2026. The joint venture targets a total capacity of 700,000 tpa. -

Black Pellets / Biocoke:

Idemitsu is considering the construction of black pellet plants in Indonesia, contributing to the region’s 3 million tpa target by 2030. -

Aisin Takaoka & Triputra:

Began producing biocoke from palm kernel shells (PKS) in West Kalimantan in December 2025. Current capacity stands at 15,000 tpa, with plans to expand to 90,000 tpa by 2031. -

Tess Holdings:

Expected to start EFB pellet production in June 2026, with capacity projected to reach 100,000 tpa by 2030.

Challenges

-

Logistics Risks:

A major jetty at Tanjung Buton Port collapsed on January 5, 2026, creating a bottleneck at a key biomass export hub in Riau, Sumatra. While the immediate impact is mainly on PKS exports, the incident highlights infrastructure risks that could affect pellet logistics if exporters are forced to divert cargoes to congested alternative ports such as Dumai.

2. Malaysia: Innovation in EFB & Premium Products

Malaysia is capturing market share by leveraging palm oil waste (EFB) and developing high-end black pellet production, diversifying beyond traditional white wood pellets.

Current Market Situation

-

Steady Growth:

Malaysian exports to South Korea increased 26% year-on-year in the first seven months of 2025. As of August 2025, exports to South Korea rose 13% month-on-month. -

Winning Long-term Contracts:

Malaysian producer Mieco Manufacturing signed a five-year supply agreement with Korean importer K-One for 160,000–200,000 tons per year.

New Plants & Production Capacity (2026 Outlook)

-

Rainbow Pellet:

Scheduled to launch a pilot black pellet plant using steam-explosion technology, with a capacity of 6,000 tpa, in Pahang in March 2026. -

Wilhelmina:

Operating a TG2 EFB black pellet plant in Kuantan, currently producing around 17,000 tpa, with maximum capacity expected to exceed 80,000 tpa. -

Kobelco & Samling:

Conducting a feasibility study for a black pellet plant in Sarawak. Construction is expected to begin in 2026, with an initial target capacity of 300,000 tpa.

Challenges

-

Rising Costs:

The Malaysian government removed diesel fuel subsidies in July 2025, increasing transportation costs by USD 5–10 per ton. Recent 30% increases in road transport tariffs and higher collection fees at mills are further pressuring FOB prices. -

Weather Disruptions:

Flooding in Peninsular Malaysia (December 2025 – January 2026) severely disrupted logistics operations and raw material collection in northern regions.

3.Thailand: Domestic Consumption Constraining Exports

Unlike Indonesia and Malaysia, Thailand poses a smaller competitive threat to Vietnam in export markets, as strong domestic demand absorbs most of its supply.

-

Export Decline:

Exports to South Korea fell 46% year-on-year in March 2025. -

Shift to Domestic Use:

Thai industries are transitioning from wood chips and pellets to palm kernel shells (PKS) for power generation, effectively turning Thailand into a net biomass importer, sourcing PKS from Indonesia and Malaysia rather than acting as a major pellet exporter. -

Market Impact:

Thailand may continue to supply niche spot volumes, but it is unlikely to replace Vietnam in large long-term contracts in 2026.

Related Posts

What is WOOD PELLET

This article discusses some of the distinct advantages and aspects of Wood Pellet that make it stand out in terms of effectiveness and sustainability. 1. High Energy Efficiency Average calorific...

Đại hội đại biểu Hiệp hội Gỗ và Lâm sản Việt Nam (Viforest) nhiệm kỳ V (2025–2030)

HIỆP HỘI GỖ VÀ LÂM SẢN VIỆT NAM TỔ CHỨC ĐẠI HỘI NHIỆM KỲ V (2025–2030) Đại hội Viforest nhiệm kỳ 2025–2030: Định hướng phát triển bền vững, mục tiêu...